I have very low confidence in most of what I read about monetary policy lately, not because I doubt the authors, but because I am not sure that the traditional tools are meaningful now. Each month I review the Bureau of Labor Statistics inflation data and cannot see how the problem items relate to short-term interest rates.

Take piped natural gas as an example. Each month recently it has been the highest or nearly the highest inflationary component of the Consumer Price Index (CPI). Year-over-year inflation in piped gas was 13.8% in the August report. Similarly high inflation items are used cars and trucks +6%, electricity +6.2%, tobacco and smoking products +6.3%, motor vehicle maintenance and repair +8.5%, and meats, poultry, fish, and eggs +5.6%. * How do high rates prevent inflation in these most inflationary elements of the index? I asked a rancher a similar question about beef and was told that there are not enough cows. Will there be fewer cows, and therefore more beef inflation, if rates are lowered?

The primary explanation that we are given for the need to lower rates concerns another area that I have low confidence in. That is weakness in the job market. I am uncertain that we can know how many jobs the economy needs when we are in the middle of dramatic changes in the immigrant workforce. How can tinkering with short rates impact a workforce that exists in the shadows and is changing by millions?

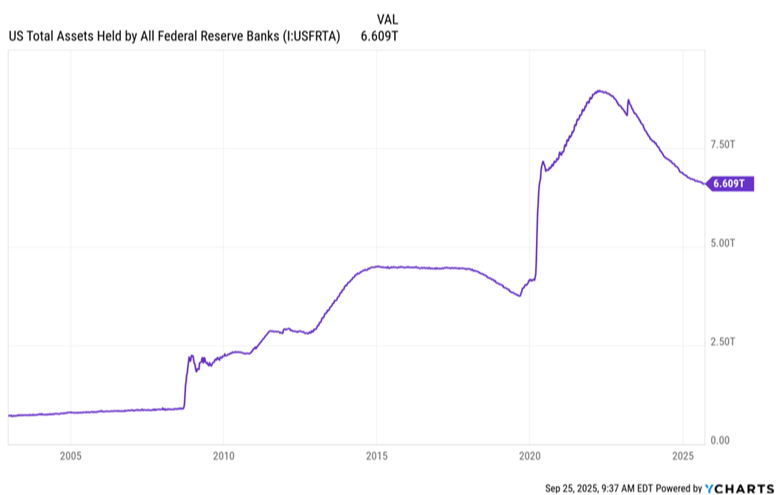

Meanwhile, nobody that I am reading discusses the other giant monetary-policy elephant in the room, which is the Fed’s balance sheet. US total assets held by all Federal Reserve banks are down by about -7.12% from one year ago. That represents roughly $550 billion of Quantitative Tightening (QT). Nevertheless, the Fed still holds about $3 trillion more in debt instruments than it did immediately before the pandemic. ** There is still a lot of QT ahead of us. The chart is below.

I am impressed that the economy is doing so well in the face of manifold complex challenges. Of course we need to concern ourselves with monetary policy, but tariffs, immigration, and fiscal policies appear to me to be more important and more difficult to analyze than 0.25% changes in the short rate. Perhaps the biggest concern should be that lower rates could lead to even more margin borrowing by speculators. As I wrote in the newsletter, I am worried about the amount of leverage being pushed by brokerage firms. Lower rates will not make that better.

* Graphics for Economic News Releases, 12-month percentage change, Consumer Price Index, selected categories, August 2025 not seasonally adjusted. U.S. Bureau of Labor Statistics. https://www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category.htm. Accessed on 09.25.2025.

** US Total Assets Held by All Federal Reserve Banks (I:USFRTA) YCharts, online September 15, 2025. https://ycharts.com/indicators/us_total_assets_held_by_all_federal_reserve_banks. Accessed on 09.25.2025.